Housing Is Broken

The last 2.5 years I spent renovating an old home. With the belief that it was a smart thing to do.

Experience taught me otherwise.

Don't renovate.

Thinking about renovating or buying an old house?

Don't do it.

It's not worth it.

Don't renovate.

The search

My interest in alternative housing started because of the global rise in housing costs.

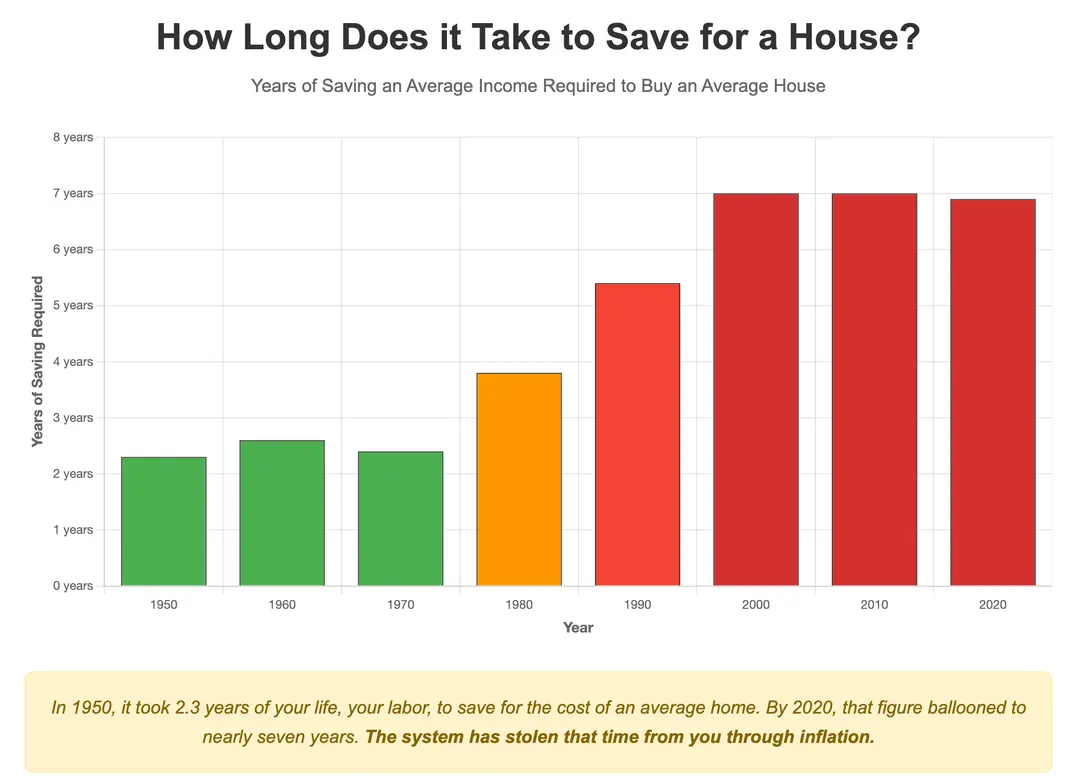

It used to take about 2.3 years of saving an average income in the 60's to be able to buy the average home.

In 2020 this ballooned to 7 years, nearly 3 times as long. Now in 2025, we're already at 8-9 years.

If you want to live in a major city like Amsterdam, London or LA, that number is closer to 11–13 years.

And the gap just keeps growing.

Meanwhile, incomes haven't kept up this pace, meaning mortgages now eat up a bigger % of our income.

And the knowledge barrier for entry level positions has risen as well in this period.

It's not a pretty picture and there aren't many great solutions.

With home-ownership comes engagement in society. You’re not just fleetingly passing through anymore, but settling and becoming a part of.

Property ownership is a proxy for economic engagement. People who own a property in a country feel a sense of ownership in their future and society. They study, save, strive and vote more than people trapped in a culture of tenancy

The Ascent of Money — Nial Ferguson

What I ultimately was looking for was just a place to live that I could call my own but not have to sign away 25-30 years of my (best) years into a mortgage that consumes 50% or more of my income.

Where the remainder of your life is dictated by a job you can't exit from (and possibly dislike), since the floor for simply existing has been raised.

Fuck that.

And so the search began:

I was inspired by the bigger-pockets forum/podcast, mortgage free living series, how to live mortgage free, never-too-small/living big in a tiny house youtube channel to find a solution to this growing problem.

To find a way to get a roof over my head without breaking the bank. To live without the ball-and-chain of crushing debt.

When it comes to alternative housing options, there are many;

- House boats

- Tiny houses

- Yurts

- Van/car living (and every modified vehicle in-between)

- Co-housing

- Prefab/convertible homes (think boxabl)

- House "hacking"

- Room & board

All different ways the millennial generation tries to cope with the rising cost of living. To reduce their footprint and convince themselves it's ok.

For example: I know a friend who has bought a house and rents out rooms in his, a friend who built a semi-mobile tiny house, another who built a prefab home and another who bought a really expensive house and now has multiple jobs with little leisure.

Trade-offs are real: Privacy, resale value, affordabillity, comfort, space, ... .

For myself, I settled on "house-hacking" since that was closest to "normal" living with the least amount of trade-offs. With most others you have to;

- Live uncomfortably small (especially in a relationship this sucks, forget about it when you have children)

- Give up on privacy (Who still wants room/flat-mates in their 30's?)

- It's hard to re-sell/build equity in most alternative housing options. High investments to a boat, yurt, van rarely pay off when selling. The market just isn't that large.

House hacking - for the non-affected boomer - is buying a larger home than you need and renting part of it out to reduce your cost of living.

This can net a lower monthly payment and higher leveraged equity compared to buying something smaller like an appartment.

It's all the rage in the US - but to be fair -houses in the US practically come for free with their cereal. It's a completely different world compared to europe. With their low/no down payment FHA loans, freddie mac, fannie mae, 1031 exchanges, ... .

But in europe - land of regulation and bureacracy - it's a bit harder. The idea is still pretty powerfull, but the rules for execution aren't the same here.

The find

Overall, I think I've gone into the decision somewhat more prepared than the average person.

- I've made checklists and spreadsheets of what is needed to estimate the condition of a building and the costs

- I created daily scrapers that continually searched the latest listings across 4 platforms for the area I was interested in. To make sure I was "first".

- Visited at least 100 houses before buying and kept track of their final sale prices. Which allowed me to narrow down on "affordable" but still "nice" regions.

- Made various rent vs buy and investing ROI calculators

But it's hard to really prep for the reality of such a project, especially without someone with previous experience.

I settled on buying a fixer-upper around 290K in a good neighbourhood.

But you quickly learn that the sale price goes up fast. Because, when you buy a house, everyone wants their cut. In no other purchase are so many parties involved that leech off this big transaction.

The notary is priced in a % of the sale, the real estate agent wants a % (event though most know nothing about houses and don't really have to "sell"), the architects' fee is a percentage of the construction costs, the government taxes are a percentage of the house cost (all building materials are marked-up as well), the contractor takes a % on top of the building materials and so-on.

It also didn't help that I bought in peak material prices 😅

With lower interest rates usually come higher prices and ultimately it's the burden of the monthly payment that's most important. It's hard to define what a "good" purchase is these days.

The execution

After buying, the reality of renovating a property in Western Europe sinks in;

Building permits take a long time. Most governments are horribly slow and inefficient. I waited 4 months just for a reply! Success seems determined by "knowing someone" in the local administration. And you can't start before the green light is given.

There are forced building "standards" these days, even if you can't pay for them. They make little sense and mostly benefit the job security of the ones writing and enforcing the policy. Like the required "safety/ecological inspectors" who don't show up, don't add any real value and cost tons of money.

Mandating something is a profitable racket to run for the otherwise unemployable - And in Europe there's plenty of those freeloaders.

You can get fined when your renovations take too much time.

Anything that can go wrong with contractors will go wrong:

- arriving late or not at all

- stealing tools

- breaking new construction

- making problems worse instead of fixing. (Most contractors don't have the full scope of the project (nor care) and just want to get their part done asap. You'll continuously have to double-check the work of the "experts" all the time, even if you know nothing about it.)

- asking payment for work not performed

- requiring full payment before starting the job

- over-charging

Neighbours that complain about everything (noise, dust, parking spots, ...) or sue you because they don't like your plans and have nothing better to do (happened to me)

And you know what's the absolute worst about a long renovation?

The chaos.

The long-lasting, life-dislocating, all-consuming renovation chaos.

That's the worst.

If - like me - you delved into this project without any prior construction knowledge you get to discover the absolute joy of making a thousand big and expensive decisions about things you know absolutely nothing about.

I'm talking 6 months of savings for 1 decision.

And if you don't decide - the project doesn't move. So at some point you just get 3 quotes, talk to the contractors and pick one. You simply don't have the time to compare everything.

I'm not sure tracking my expenses in this period was a net positive in this period 😅

The impact is unmatched:

- Your car or clothes will rarely be clean - ever

- Your health will deteriorate trying to squeeze in meals and sleep next to the construction work

- Your relationships deteriorate. Makes me wonder about the correlation between breakups and renovations. Worst case is if you're pregnant/have a young child, that's a recipe for disaster.

- No time to think about anything else. It's a full-time job next to your full-time job. Everything else besides the renovation gets derailed.

- Chaos impact. At many points in the project you don't really have any time/energy to really plan ahead (no time to think/control costs). Since your job is two-fold:

- Figure out which work/materials/contractors are needed

- Ordering/planning and executing said work. Making sure everything and everyone is at the right place, at the right time

- Motivational impact. You just have 1 huge goal that doesn't fucking move forward. You're not able to get the satisfaction of small wins. Or at least for me this wasn't the case.

- Chronic stress over a longer period lowers your ability to handle other stress

Oh yeah - Did I already mention the financial stress?

Did I mention this? 😅

So here's the TLDR;

Don't be stupid. Save your time, effort and sanity and just start a business instead, the upside is much much larger.

Don't buy - Don't renovate.

If you're single, a compact & mobile tiny-house or van home is probably the right answer to the housing problem right now.

Or still doing a house-hack, but in a way that less renovation is needed. Something that's already decent and can be rented-out as is. Where you just rent out other rooms of an older house/appartment and sacrifice some privacy and living standard/comfort.

If you're a couple, the answer is probably to rent small, live light, don't buy expensive furniture, reduce your cost of living, possibly move to a lower cost of living area/country where you can earn and save more and forget about owning.

Put the rest in a whole-world ETF stock portfolio and gold/bitcoin if you expect high inflation. Don't let your savings sit idle on savings account. Putting money in a low-yield savings account is like holding melting ice cubes. Each year 10-15% of your purchasing power gets robbed.

Consider carefully if renting/living lighter isn't the better decision. Owning, from my experience, is not the solution, it's just a different kind of trapped. The property ladder doesn't lean against a wall worth climbing.

Spend your life on what matters instead of investing time, energy and your savings in asbestos-infested infrastructure of the previous generations.

Which is ultimately still pseudo-owned by the bank and government.

The result

In the end (after 2,5 years of work and a ton of money) it did work out though.

We had this modern, private 1-bedroom appartment right outside a big city with a garden all to ourselves, two good incomes and the rental part was paying the mortgage.

I learned a ton by diy-ing many of it (deconstruction, plumbing, electric, drywalling, painting, installing kitchens/bathrooms/cabinets, 3d modelling ...)

But it wasn't worth the struggle.

Should've just bought a van/tiny-home and park it somewhere and focus on starting a business. The chances of a good ROI on that are just so much higher.

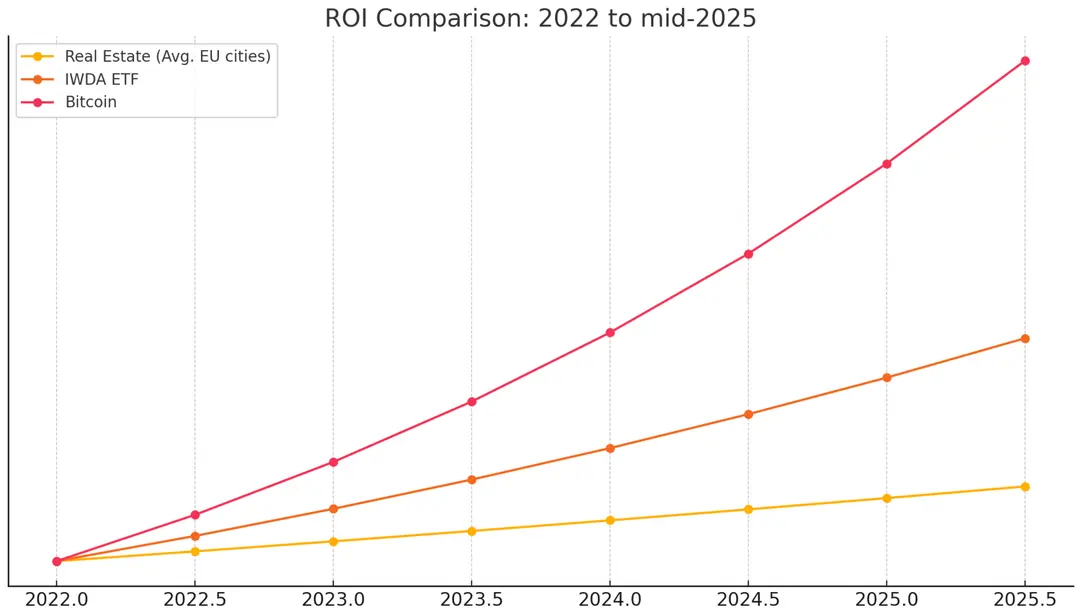

If I had put the money in the stock market or bitcoin I probably would've been better off. Even with the leverage-effect of loaned money.

Here's the comparison of putting the same amount of money in IWDA or BTC over the last 3 years compared to real estate:

- Real Estate (based on average returns in major EU cities like Berlin, Amsterdam, Brussels ~6%/year),

- IWDA ETF (global equity, ~14.2% annualized),

- Bitcoin (~28.5% annualized, reflecting historical gain over that period).

But off-course, buying a house isn't just a financial decision. It's as much a life-quality decision and you have to live somewhere.

Or maybe your mileage will vary and I'm to blame for just general bad decision making.

Or it was just bad timing and this would've been a brilliant idea at a different moment in time. Right place wrong time kinda thing.

Or maybe it was a good idea and I just need more time to forget about the chaos/struggle and let the benefits accumulate over time.

Maybe I'm just an idiot

All of the above are very probable.

Tips

If you're mentally insane (or soon-to-be). And still end up renovating. Here are some pro-tips:

- Live close to the site

- Don't do it in any big city (it is nearly IMPOSSIBLE to get rid of garbage or even park construction vehicles. Let alone get the permissions in place on time)

- Don't do any work that requires a permission. Or better: don't ask for the permission but do it anyway. Easier to ask for forgiveness. Especially in rural places you can get away with this.

- Befriend your neighbours, or don't have any. You could avoid lawsuits at least. Watch out for older people with too much spare time and money on their hands. They don't like change. NIMBY is a thing.

- Have at least 100k set aside or borrowed. It doesn't matter what you think it will cost.

- Don't do it whilst having a young child/being pregnant. There's a high correlation of renovation/construction/building break-ups. It's a stress-combo of death.

- Aim to make it last for 6 months max. This way the project will stay under a year. You always find out more shit that needs fixing once you start ripping up the building.

- Ideally have a friend/family member in construction that can guide you/lower the total price

- Have a general contractor you can work with for the full project. "A general renovator" who can help oversee/chunk the project. Pay this guy per hour and buy the materials yourself. Be sure he's critical and asks good questions. Be sure they are fed, have drinks and as much caffeine as they want. Make sure all materials are on-site when they arrive so they can focus on what you can't do.

- Do deconstruction yourself. It's the easiest cost saver. Round up some friends, get some sledgehammers and pizza's and hammer time!

- Use architects only for a plan - They are mostly incentivised to increase the total price of the renovation.

- Negotiate a good bank deal. Be willing to switch banks. Go for fixed rates in high inflation environments. Ask for a 100% loan if possible.

- Find a good construction material supplier who gives you contractor prices if you buy all materials with him.

Conclusion

Lastly I want to address the real root cause of the problem:

And that is that people use real estate as a store of value. Housing is broken because our money is broken.

Inflation is high, bank accounts yield nothing so surplus savings flow to safe, hard assets.

Real estate, art, stocks, watches, gold/silver, fancy cars. All utillity objects that get over-valued because saving for the future is just broken.

The "monetisation" of real estate adds a premium on top of the utillity value that a house provides. Making it more expensive than it needs to be. It becomes a piggy bank instead of a tool.

It's seen as an investment instead of a depreciating asset; Pushing people who need a roof out, by the ones who need a place to park their wealth.

Over time when we'll make the transition from weak to stronger money, the monetary premium will be drained from real estate and prices will eventually come down again to normal levels.

Just be sure not to be left holding the bag with a large property portfolio, high mortgages and depressed rental/purchase prices.

But who knows how long that will take?

There's no use in complaining about the way the world is. Make the best of it and play the cards you've been dealt.

Do something instead of sitting on the sidelines never taking action. Sometimes doing the wrong thing is better than trying nothing.

Low cost of living, high agency, self-taught skills, flexible income sources, smart investing and abillity (+ willingness) to relocate are key attributes for our generation to thrive in troubled economies.

Stay optimistic. Choose hope. Choose better money

Comments/Questions